You've reached the Virginia Cooperative Extension Newsletter Archive. These files cover more than ten years of newsletters posted on our old website (through April/May 2009), and are provided for historical purposes only. As such, they may contain out-of-date references and broken links.

To see our latest newsletters and current information, visit our website at http://www.ext.vt.edu/news/.

Newsletter Archive index: http://sites.ext.vt.edu/newsletter-archive/

The Personal Finance Scorecard: Your Annual Check

Farm Business Management Update, December 1998

By David M. Kohl and Alex W. White of the Department of Agricultural and Applied Economics, Virginia Tech

Many people have a tendency to postpone scheduling their annual check-up with the dentist. The results sometimes can be painful, both physically and psychologically, and can hurt the pocketbook. The same feeling, though not physical, can be experienced in your personal finances. Professional financial planners recommend a complete analysis of personal finances annually. A checkup allows an individual to be proactive rather than reactive in developing a plan for corrective action. The result is financial success and independence now and in the future.

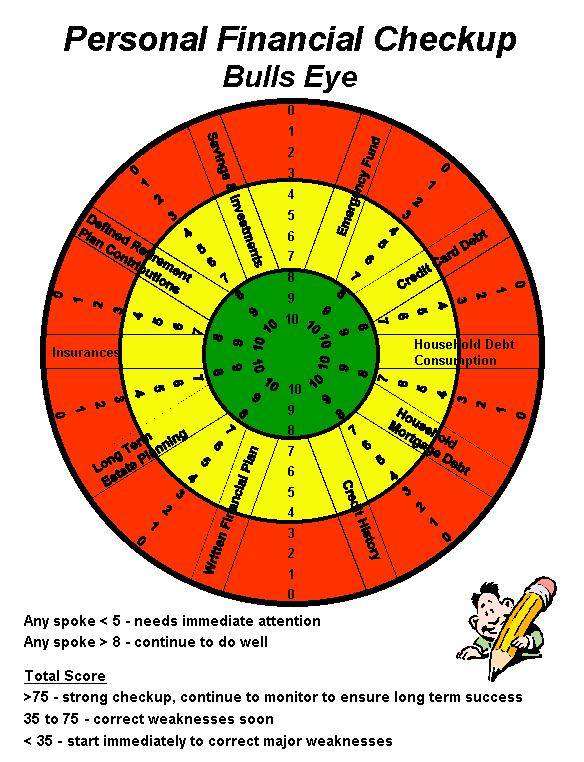

An extensive personal financial analysis includes examining a wide spectrum of criteria, ranging from the cash emergency fund to credit usage, investments, insurance, and long-term estate planning. Following is a ten-point checklist to evaluate your current financial position. Age, personal and family circumstances, and goals can influence the interpretation of the results.

The analysis of each criterion will be analogous to a stoplight (Figure 1). A green light, a score between eight and ten, generally indicates strength or progress. A yellow light with a range of four to seven usually denotes some weakness and the need for corrective action. A score of zero to three suggests major weakness and the need for immediate corrective attention. While general guidance in ranges is provided, you must determine the specific ranges.

Overview: Criteria and Components of Scorecard

Emergency Funds

One of the first steps to financial security is to build a personal or family emergency fund. This fund includes all cash assets that could be turned into cash quickly, without disrupting your normal lifestyle. Cash in checking and savings accounts, cash value of life insurance, and CDs and money market funds that can be withdrawn without penalty qualify. The emergency fund would not include available credit lines on home equity loans or credit card debt. If you become unemployed or have a tragedy, these sources of credit could be eliminated quickly.

To determine your emergency reserve, divide the cash assets by your monthly gross salary or net income, if you are self-employed. Three months reserves or more would indicate strength. One to three months denotes some vulnerability. Less than a month or no cash reserves means possible financial stress if an unexpected emergency should occur. Size of mortgage, job security, and personal debt obligations may influence the interpretation. The average American has less than one month's reserve.

Credit Card Debt

According to "Money Section" of the November 12, 1998 issue of USA Today, individuals who have outstanding balances on credit cards typically have a total balance of nearly $6,000. And, this balance is spread over 14 different cards.

If the total balances on your credit cards exceed 15 percent of your gross income, you are in the danger zone. Five to 15 percent represents caution, and less than 5 percent would place you in the safe category. Time of year and past reputation of repayment of credit cards may influence interpretation.

Household Consumer Debt (Excluding Credit Card Debt)

The next step is to add up all payments of household obligations: car, appliances, college tuition debt, and any payments to family or friends. If the total payments exceed 15 percent of gross salary or net business income, you are in the danger or red light zone; 5 to 15 percent suggests caution or yellow light zone, and less than 5 percent is the green light zone or a strong position. Usually young people who have no mortgage will have a higher ratio.

Credit History

Every two years, you should request a report of your credit history. You can make the request through the major reporting agencies such as Equifax for $8. Lenders are placing increased emphasis on these histories in customer acceptance and denial of credit. If you have a history of delinquent payments, repossessions, or bankruptcy, you will experience a high degree of difficulty in obtaining credit, and you will probably be charged higher interest rates. Minor delinquent payments on credit cards or financial problems would result in some degree of caution by lenders. If you have a history of being current on payments and have not filed bankruptcy, you are in a strong position to negotiate for credit and interest rates.

Savings and Investments

At the other end of the spectrum, you should analyze savings, investments, insurance, and long-term estate and financial planning.

If you are saving more than 5 percent of your gross salary or net business income in investments over and above retirement plans at work or business, you are in a strong position. One to 5 percent indicates that you need to increase your savings, while no saving or withdrawals from long-term savings indicate danger. Age and income levels and retirement goals may result in different ranges on the scorecard.

Retirement Plans

Many individuals have defined plans such as 401-K and 403-B through work or SEP, IRA, or Keogh plans as a result of owning a business. The choice of investments in these plans range from stocks and bonds to mutual and money market funds.

When you invest more than 5 percent of gross salary or net income in these accounts, you are considered in the green light zone. One to 5 percent would indicate yellow light zone and a need for increased contributions. Zero percent or withdrawal from these funds may result in insufficient retirement income, particularly if one has little invested in Social Security contributions, and is a decided red light.

Insurances

Insurance represents a risk management tool. Some people desire self-insurance with no formal insurance plan. Others are more risk adverse and seek a comprehensive insurance plan. Age, family needs, health, and goals and objectives will influence individual insurance levels needed.

If you have comprehensive medical and health insurance, life, disability, liability, renters or homeowner policies, and long-term health care, you would be in a position to handle most risk. You need to revisit your insurance plan every five years.

Lack of some insurance components may mean that you should shore up weaknesses. Self-insurance in some of these areas could make you vulnerable to unexpected disasters or loss of earnings, wealth, or equity.

Estate Plans

One component of personal finance plans that people often procrastinate in doing is formal estate planning. If you have a written will or comprehensive estate plan that is updated every five years, you are in a strong position or the green light zone. A partial plan or lack of a will places you in the yellow or red light zone for your checkup. This means you are placing your family and heirs in more financial risk.

Written Financial Plan

Personal financial plans need to be written with goals, objectives (short and long run), evaluations, and measurements. Statistically, a written plan is more likely to be achieved.

A personal financial plan has many facets. Credit, investment savings, insurance and protection of assets through an estate plan are the cornerstones. The real test is to examine your strengths and areas for improvement through the scorecard. Only by going through this process can you really identify what areas you need to target to insure the financial health and well-being of you and your family.

Complete the Scorecard Checkup

Contact David M. Kohl at sullylab@vt.edu and Alex W. White at axwhite@vt.edu .

Visit Virginia Cooperative Extension