You've reached the Virginia Cooperative Extension Newsletter Archive. These files cover more than ten years of newsletters posted on our old website (through April/May 2009), and are provided for historical purposes only. As such, they may contain out-of-date references and broken links.

To see our latest newsletters and current information, visit our website at http://www.ext.vt.edu/news/.

Newsletter Archive index: http://sites.ext.vt.edu/newsletter-archive/

Financial Analysis of an Agricultural Business - the Job-Cost Estimate

Farm Business Management Update, June - July 2007

By Alex White (axwhite@vt.edu), Instructor, Agricultural Finance and Small Business, Agricultural and Applied Economics, Virginia Tech

My last article discussed the basics of enterprise budgets – what are they, why you need them, and how you use them. This issue will focus on a similar statement – the job-cost estimate. Job-cost estimates are very popular in the landscaping and contracting industries, but they can be very useful tools for any agricultural business.

A job-cost estimate lists the expenses related to a specific activity or “job.” For example, a landscaping firm might use a job-cost estimate to determine how much it will cost to design and install a residential landscape project. A greenhouse operator might use a job-cost estimate to determine all of the expenses involved in holding a special event such as a customer appreciation day or an educational seminar series. A pumpkin producer might use a job-cost estimate to estimate the costs involved with a pumpkin festival.

Besides helping a producer determine and estimate all of the expenses related to a certain “job,” a job-cost estimate also helps you determine the price you will need to charge for doing that job. Further, a job-cost estimate provides information that will help you determine your breakeven level of sales.

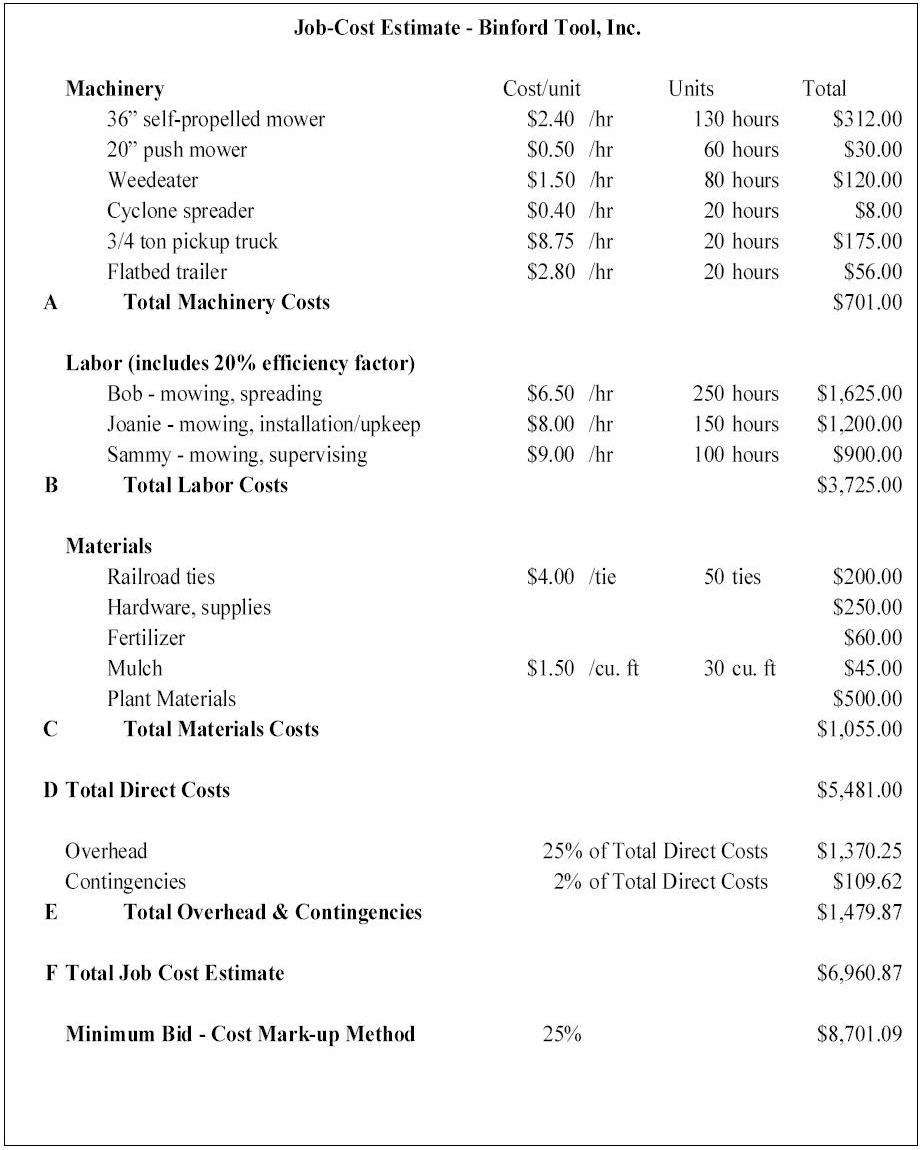

Everyone who uses a job-cost estimate has a slightly different format, but a job-cost estimate has five basic sectors – Machinery Expenses, Labor Expenses, Materials Expenses, Overhead Expenses, and the Price Estimate section. A sample job-cost estimate is available at the end of this article. Again, there are several formats for a job-cost estimate – most managers start with the basic format and then tailor it to fit their specific operations.

The Machinery Expense section lists all of the machinery or equipment that will be used in completing the job. For example, a landscaper may need a skidloader, trencher, truck, and trailer to install a landscape design. The Machinery Expense section for this job would list the following information:

This list will help you think through all of the different types of machinery and equipment needed to complete a job. It helps you schedule the order of operations, as well as the availability of equipment. For example, you may determine that you will need to rent a certain piece of equipment to complete the job.

There are two main formats for the Labor Expense section. One method is to list the types of labor needed to complete the job (the “activities”). For this method, you would list all of the activities the labor force would be doing – mowing, raking, installation, customer service, etc. The second method is to list the workers who will be involved in the job – 1 manager, 4 workers, etc. Regardless of which method you choose, you list the following information in this section:

For example, a greenhouse operator determines that he/she will need four workers to successfully hold a Customer Appreciation Day event. Each worker will be used for eight hours, and the hourly cost of each worker is $20/hour. The hourly cost includes cash wages as well as FICA and FUTA costs, worker’s compensation, and any perks paid to the worker. A rough rule of thumb is that your actual total labor costs (wages, FICA, FUTA, etc.) are generally 150% of the cash wage. For example, if you are paying a worker a wage of $10/hour, that worker is costing you approximately $15/hour after all other non-wage labor expenses are included.

A little tip I learned about estimating the labor involved in a job – add a 20% efficiency factor to most of your estimates. This 20% efficiency factor will account for time the employee is actively on the job, as well as the time they are setting up, cleaning up, or on breaks. For example, a lawn care manager may estimate that a worker will need 5 hours to mow a yard. But you need to realize that the worker is “on the clock” while he is loading the mower onto the trailer, driving to/from the worksite, eating lunch, and refueling or repairing the equipment. For that reason, you should list 6 hours (5 hours mowing x (1 + 20%)) labor on the job-cost estimate.

The Materials Expense section is probably the easiest section to complete. This section is simply a list of the materials needed to complete the job and the associated cost. For this section you list:

You may include sales tax in your material cost, or you may list it separately – but be sure to include the sales tax in your job-cost estimate.

Total Direct Job Costs are determined by totaling the machinery, labor, and materials costs. One way to regard Total Direct Costs is that these are the “out of pocket” expenses or the variable costs of completing the job.

Overhead expenses are those expenses that cannot be directly attributed to one particular job. Examples of overhead include rent, administrative salaries, business licenses, insurance premiums, and office utilities. It can be hard to estimate how to allocate a portion of a business’ overhead expenses to a particular job; therefore, most operators use a percentage of overhead expenses for each job. For example, if you think you will have 10 relatively similar jobs per year, you include 10% of the annual overhead expenses in each job-cost estimate.

Other items that can be included in the Overhead Expense section are guarantee costs and contingency costs. A guarantee cost estimates how much it might cost a business to repair or replace a defective product. For example, a landscaper may guarantee all plants for up to one year. If a plant dies before the one year is up, the landscaper must replace that plant. Most firms typically use a percentage of the total plant expenses as a guarantee cost.

Contingency costs are basically “what if” costs. What if we underestimated the amount of materials or labor needed? What if the cost of the materials is higher than expected? What if you forgot to include a material or piece of machinery in the job cost? Again, contingency costs are usually estimated at a percentage (for example, 2%) of the total direct costs of the job.

Once all of the above expenses are estimated, simply total them to determine the Total Job Cost. This is your best estimate of the direct (variable) and indirect (overhead or fixed) costs related to a specific job. This figure represents the total cost of completing a job, and it also represents the minimum price that you should charge, or bid, for a job. There are several methods of determining the actual charge or bid for a job. The most common method is the “Cost Markup” method. For this method, you determine the appropriate cost markup percentage to use. This markup percentage varies by industry and location – there is not a set percentage to use. You must determine the appropriate percentage to use for your business and your customers.

The cost markup method is quite simple, once you have determined the cost markup percentage. Simply multiply your Total Job-cost estimate by (1 + Cost Markup Percentage) to determine your final price or bid for the job. For example, assume that your Total Job-cost estimate is $5,000, and your cost markup percentage is 25%. Your estimated charge for the job is calculated as follows:

$5,000 x (1 + 25%) = $6,250

This charge of $6,250 is intended to cover all of your variable costs (Total Direct Costs), a portion of your annual fixed costs (Overhead), a portion of any guarantee or contingency costs, and provide some profit to the business. Again, you will have to determine your cost markup percentage on your own.

Job-cost estimates are powerful tools for a wide variety of businesses. I have seen examples of job-cost estimates in the landscaping, lawn care, construction, and consulting industries. But I think that job-cost estimates can be powerful tools for agri-tourism, wholesale or retail greenhouses, and for special events (livestock sales, open houses, seminars, etc.) at any agricultural business.

If you would like to receive an Excel spreadsheet with a basic job-cost estimate, please contact Alex White at axwhite@vt.edu, or call Jill at (540) 231-7727 and leave your contact information. You can also go to my new (and still under construction) website at http://faculty.agecon.vt.edu/alexwhite/ to download a job-cost estimate spreadsheet.

Visit Virginia Cooperative Extension